What Microsoft and Chevron Left Out of the Pecos Headlines

Project Kilby is being sold as an AI-infrastructure milestone and a community-first investment. It is also the largest oil-major / Big-Tech power deal yet, an elegant route around both the Texas grid

On Monday, June 22, Microsoft announced one of the largest single capacity additions in its history: a roughly 2-gigawatt data center campus in Pecos, in far West Texas. The company says the multibillion-dollar build will span the next five to seven years, support more than 6,000 construction jobs at peak, and create hundreds of permanent operational roles. The blog post by Noelle Walsh, president of Cloud Operations and Innovation, reads as community reassurance: clean energy, no increase in local electricity bills, almost no water use, and a “Community First” approach. All of it sits under Microsoft’s standing 2020 pledge to be carbon negative by 2030.

Not Pecos — this is Microsoft’s existing Arizona data center campus, the kind of build the company says Pecos will resemble. The power behind the new one, and the gas, come from Chevron under a 20-year deal. (Image: Microsoft)

Read the Chevron release that landed the same morning, and a different, more revealing story emerges. Microsoft didn’t just announce a data center. Chevron announced its entry into AI infrastructure at scale, and the structure underneath the deal, the part neither company puts in its headline, is the actual news.

One thing up front: this is not a hit piece, and there is real strength in what Microsoft is doing here. But if you take away only one line, take this one. The headline is about AI, but the durable asset being created is a 20-year, oil-price-independent gas annuity, and the party holding it is Chevron.

The deal they didn’t put in the headline

The power for Pecos comes from Project Kilby, a 2.67 GW natural gas plant that Chevron, according to its own release, will build through a wholly owned subsidiary, Energy Forge One LLC, under a 20-year power purchase agreement. The way the two announcements are framed is already telling: Microsoft’s blog never names Chevron (The Register flagged this), and Chevron’s release refers to “West Texas” and Reeves County but not to the city of Pecos itself. Microsoft only admits the facility “will operate with a co-located natural gas power facility,” and confirmed to The Register that the two are the same project. Put the releases side by side and the shape is unmistakable: dedicated, behind-the-meter gas, by both companies’ accounts not connected to the public grid, sized at 2.67 GW to serve a campus of roughly 2 GW.

Several details matter, and none of them appears in Microsoft’s letter to the community. The deal’s co-developer is the activist investment firm Engine No. 1, working through its energy company Joulent, which was founded by the same Chris James of Engine No. 1; per Bloomberg, the firm holds an option to take half of Project Kilby’s ownership and contribute a matching share of the capital. Most of the generation comes from large GE Vernova turbines, with Chevron and Engine No. 1 securing seven GE Vernova 7HA units (each offered in 290, 384, or 430 MW configurations; seven of the 384 MW model alone get you to about 2.69 GW), and the balance comes from Solar Turbines, a Caterpillar subsidiary. That name is worth noting: Solar Turbines also supplied the turbines for xAI’s Colossus facility near Memphis, an installation of roughly 150 MW that is currently the subject of a lawsuit over local air pollution, and by The Register’s math Kilby is about eighteen times the size of that Memphis plant.

Chevron hasn’t disclosed an official cost, but people familiar with the deal put it near $7 billion; the company is targeting mid-teen returns and describes the cash flow as “diversified” and “independent of oil and gas price cycles.” Chevron expects a final investment decision (FID) by the end of 2026, after permitting, with first power in 2028 and full build-out continuing into the 2030s. The site spans more than 2,000 acres in Reeves County, near Verhalen, southeast of the city of Pecos and roughly an hour from Odessa, and, importantly, close to the Waha Hub (why that matters comes below). Chevron’s VP of power, Daniel Droog, put it plainly: the project will “create another significant demand source in the Permian Basin,” and “it’s hard to beat the Permian.” Chevron values the plant’s economics at more than $10 billion in state and local tax revenue and about 2,000 jobs, and those are figures for the plant itself, separate from the data center’s jobs. The only emissions control named is Selective Catalytic Reduction (SCR), which reduces but does not eliminate nitrogen oxides, along with noise and light mitigations; carbon capture is mentioned nowhere in either release.

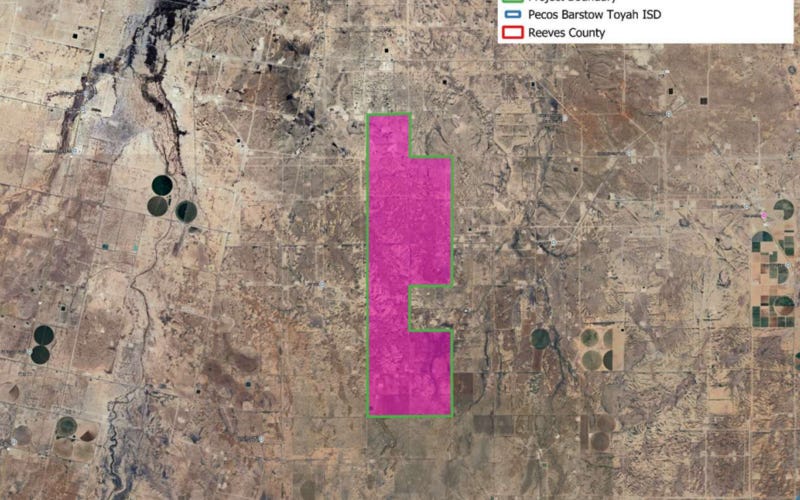

Where it lands: the Project Kilby site (magenta) in Reeves County, near Verhalen, southeast of Pecos — off Highways 17, 285 and 10, shown against the Pecos-Barstow-Toyah ISD. (Source: Energy Forge One JETI application (Texas Comptroller, J0022)

Chevron’s New Energies president, Jeff Gustavson, framed the strategy as linking “traditional strengths to emerging demand.” Droog confirmed Kilby is Chevron’s first opportunity to co-locate generation with a data center, and that the company is already in talks with other developers. In other words, this is a template, not a one-off, and that’s the lens for everything that follows.

This was telegraphed for over a year

One recurring theme of this newsletter is that the biggest infrastructure moves are usually visible well in advance if you watch the right filings. Kilby is a clean example. In January 2025, Chevron and Engine No. 1 announced a partnership to develop up to 4 GW of gas-fired power for data centers nationally. By October 2025, Chevron’s subsidiary Energy Forge One had filed an air-permit application with Texas regulators (the TCEQ) for the plant — listed there at about 2,595 MW — and in November Chevron publicly named West Texas as the site. In April 2026, Chevron, Microsoft, and Engine No. 1 signed an exclusivity agreement, disclosed in Chevron’s first-quarter filing (Form 8-K); the roughly $7 billion figure was already circulating then. And on June 22, 2026, the definitive 20-year PPA was announced.

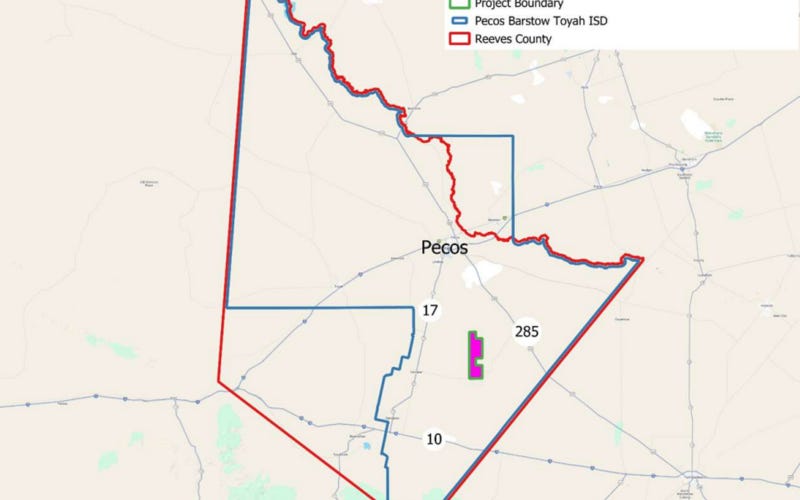

The footprint, on the ground: 2,000+ acres mapped as the project boundary — from the public filings that predate the June announcement. (Source: Energy Forge One JETI application (Texas Comptroller, J0022)

None of Monday’s news required a crystal ball: the pieces had been on the table for eighteen months. That matters for how much weight to give Chevron’s “speed and certainty” pitch. This was a long, deliberate build, not a rapid response.

Why everyone is suddenly building their own power plant

Kilby doesn’t exist in a vacuum. It’s part of a structural shift toward behind-the-meter (BTM) power for data centers, and the surrounding numbers explain why Microsoft made this choice.

Demand is surging. BloombergNEF expects U.S. data center capacity to roughly double, to 77 GW by 2030. Microsoft alone plans about $190 billion in capital expenditures this year (up 61% from 2025) and intends to double its data center footprint over two years.

The grid can’t keep up on the timelines these companies need. By the end of 2025, ERCOT, the Texas grid operator, had roughly 226 GW of large loads stacked up in its interconnection queue, nearly quadruple the figure a year earlier, with about three-quarters of it coming from data centers. Getting to the front of that queue takes years, so developers increasingly skip it: by Cleanview’s count, about 46 U.S. projects are planning roughly 56 GW of behind-the-meter capacity, around 30% of the entire planned national buildout. Kilby is large but not unusual. Cummins signed a near-identical on-site gas deal of about 2 GW with Circe Energy in West Texas just six days before the Microsoft news, Pacific Energy announced a 5 GW off-grid project in neighboring Pecos County back in August 2025, and Microsoft itself leased about 700 MW from Crusoe’s Abilene campus in March 2026.

The equipment suppliers confirm the same picture from their side. GE Vernova’s data center orders in the first quarter of 2026 alone exceeded its entire 2025 total, and its contracted gas gigawatts jumped from 83 to 100 in a single quarter. Caterpillar’s power-generation segment kept growing, and the company disclosed a new 2.1 GW agreement, its sixth of at least a gigawatt. Both companies’ shares have risen sharply over the past year. This is a genuine industrial supercycle, and Chevron is now plugging into it.

Where Microsoft is right: a strong, expensive move

Give Microsoft full credit on one point: the strong move deserves to be named before the weak ones.

By funding its own dedicated behind-the-meter generation instead of drawing from the public grid, Microsoft removes the single biggest reason data center projects are dying across the country: local fear of higher electricity bills. That fear is not unfounded. As capacity scales, the cost pressure is real and already showing up on consumer bills, and the political backlash has teeth: dozens of U.S. data center projects were killed in 2026, often with bipartisan opposition, and the recurring flashpoints are exactly electricity costs and water. By paying for its own power, Microsoft steps out of that fight; it can credibly tell Pecos the campus won’t raise local rates, because it isn’t drawing from their grid. Chevron reinforces the point: in Gustavson’s words, the plant is designed so there’s “really no competition with local electricity consumers.”

There’s a second, less-discussed reason behind-the-meter is smart here: it’s a hedge against regulation. Beyond letting Microsoft jump the interconnection queue, a self-owned, islanded plant insulates it from a whole category of future risk, such as a state or federal tax on grid consumption (one was floated in Virginia) or a reliability-driven pause or moratorium on large grid loads under some future administration. Owning your own generation is a durable hedge in case the rules change.

And there’s the Texas-specific angle, which is worth explaining carefully. In June 2025, Governor Abbott signed a large-load law, SB6, that tightened the rules for giant grid-connected loads (a large load is defined as 75 MW or more at a single site). In particular, under PURA §39.169, arrangements in which a new large load sits on existing generation and nets it against consumption now require an ERCOT study and approval from the regulator (PUCT). Here’s the key detail: that rule is written against pulling existing generation off the grid, and Kilby is new, purpose-built generation that serves only Microsoft’s load and, at launch, doesn’t export to the grid. New generation registering after September 1, 2025, isn’t subject to that pre-approval. In other words, by its very design Kilby doesn’t trip the provision SB6 was written to police. The structure also sidesteps the federal overlay tightening around co-location in other markets: FERC has no jurisdiction in ERCOT, so everything playing out in PJM doesn’t reach West Texas. For this deal, Microsoft and Chevron picked the cleanest regulatory environment in the country, and they did it on purpose.

This is an expensive, well-engineered move, and Microsoft is right to make it. Now to the parts that don’t survive a check against the source documents.

Where it’s weak: three axes, and how to fix each

The reassurances in Microsoft’s community letter are where realism has to kick in. They sag along three axes: clean energy, emissions, and water. For each, I’ll add what would make the claim honest.

1. “Clean energy” is an accounting match, not the actual power

Microsoft wraps the project in sustainability language, citing the 4.7 GW of renewables it has contracted in Texas and its 2030 carbon-negative goal. But it’s worth understanding what those renewables are. The company’s approach is to match its electricity consumption with purchases of renewable energy: certificates and contracts sourced wherever they’re cheapest on the grid. Globally, Microsoft has contracted 34 GW of carbon-free electricity across 24 countries, eighteen times its 2020 level. These are real contracts, but they are an accounting layer; they don’t change the molecules flowing into Pecos.

The Pecos campus is physically powered by gas, while the renewable certificates are bought elsewhere. That’s where the headline and the hardware diverge. And the green accounting itself is getting shakier: Microsoft is now considering delaying or abandoning its goal of matching 100% of its hourly electricity use with renewables by 2030, Bloomberg reported in May.

What would fix it: the honest move would be to stop calling the power for this specific campus “clean energy,” and to say plainly that Pecos runs on gas while the certificates are a separate, company-wide offset. Alternatively, cover part of the load with actual local renewables plus storage, rather than certificates from the other side of the grid.

2. The emissions are real, large, and aimed at the one number that was improving

This is a real plant burning real fuel, and for once there are hard third-party numbers. The Environmental Integrity Project estimates that Project Kilby could emit more than 13 million tons of carbon dioxide a year, plus 3,200 tons of criteria air pollutants and 278,000 pounds of hazardous air pollutants. The emissions control Chevron emphasizes, selective catalytic reduction, works on nitrogen oxides (a local air-quality issue), not carbon; there is no carbon capture in the project and no stated date for adding it.

Set that against Microsoft’s own sustainability reporting, and the contradiction sharpens. Per the 2025 Environmental Sustainability Report (covering fiscal 2024, against a 2020 baseline), the company’s total emissions (Scope 1, 2, and 3) are up 23.4%, even as energy use rose 168% and revenue rose 71%. But here’s the part that matters more: Scope 1 and 2 emissions (direct emissions plus emissions from purchased energy) Microsoft has cut by roughly 30% over that period, precisely through its carbon-free electricity purchases. That’s the one category where the company has real progress. A new 2.67 GW gas plant hits exactly that category: under the deal’s structure, the plant’s combustion emissions are emissions from energy Microsoft purchases, the very ones it has been driving down, and which it will now “cover” on paper by matching this load with renewable certificates bought somewhere else. The atmosphere takes on 13 million tons of CO₂; the report shows a matched, net-zero line. That is the precise mechanism of the spin.

What would fix it: either a public date by which the plant gets carbon capture (or otherwise brings its real emissions to zero), or an honest acknowledgment that the carbon-negative-by-2030 pledge and a new gas plant can’t both be live at once.

3. The water claim measures the easy half

Microsoft’s most quotable line is that the data center’s lifetime water use will be a fraction of what a single fast-food restaurant uses in a year. That’s true, but it measures only the data center’s closed-loop cooling system, which Microsoft genuinely has engineered for very low water use (its chip-to-chip liquid cooling reportedly saves about 125,000 cubic meters a year per facility versus evaporative cooling).

But the data center is half the system. The 2.67 GW power plant needs water too, and Microsoft’s flattering comparison says nothing about it, while Chevron’s release does: Kilby will run on non-potable, brackish groundwater. In drought-stricken West Texas, that’s not a throwaway detail. As The Register noted, desalinating brackish groundwater has already been proposed as a drinking-water source for Pecos and the surrounding area. So the optimistic figure covers the data center, while the larger and more contested draw, the plant’s, sits in the fine print of the other company’s release.

What would fix it: disclose the actual water figure for the plant itself, not just the data center, and commit to using treated produced water (which Chevron is piloting right next door, more on that below) rather than competing for the region’s future drinking-water supply.

And there’s one more layer that leads straight to the deal’s winner: the Permian produces more than 22 million barrels of produced water a day, and the industry is racing to turn that oilfield wastewater into a usable resource.

The trade underneath: Chevron, Waha, and stranded gas

Strip away the AI framing, and Project Kilby is at its core a 20-year gas trade, and understanding why it’s such a good one for Chevron matters more than anything else. It comes down to a single word: Waha.

The Permian Basin is primarily about oil, but it produces enormous volumes of gas as a byproduct: about 27.6 billion cubic feet a day in 2025, roughly a quarter of total U.S. demand, with the EIA projecting around 29 in 2026. The problem is that pipelines out of the basin can’t carry it all, and when the gas has nowhere to go, its local price falls below zero. The benchmark, the Waha Hub in West Texas, spent much of 2026 in negative territory: producers were paying others to take their gas. The numbers are striking. Daily Waha prices closed below zero 49 times in 2024, 39 times in 2025, and a record 87-plus times so far in 2026, including stretches of dozens of consecutive negative days; in April 2026 the average was about negative $5.66 per MMBtu, against a five-year norm near positive $3. Put simply: oil producers in the Permian are happy, while the gas has nowhere to go and is essentially being given away.

Relief is coming, but slowly. Kinder Morgan’s Gulf Coast Express expansion (about 0.6 Bcf/d) entered service around June 9, 2026, and nudged near-term prices up; Energy Transfer’s Hugh Brinson (1.5 Bcf/d) is expected late in 2026, with more capacity in 2027. But forward prices stay negative through 2026 and into 2027, and production keeps climbing, especially with oil above $100 during the Iran conflict, which incentivizes still more drilling and therefore still more associated gas.

This is the context that makes Kilby brilliant for Chevron. A co-located 2.67 GW gas plant is a permanent local consumer of gas. Taking the same 13-million-ton CO₂ estimate as a starting point, at full load the plant would burn on the order of 0.6 billion cubic feet of gas a day, molecules that would otherwise need a pipeline that doesn’t exist, or get flared, or sell for less than nothing. Behind-the-meter co-location isn’t just a regulatory workaround; it’s a way to re-price stranded associated gas. Chevron converts gas that is frequently negatively priced into a 20-year contracted cash flow that doesn’t depend on oil prices, at mid-teen returns. The company’s own phrase says it outright: “diversified cash flow independent of oil and gas price cycles.” Pipelines fill and empty, but a dedicated plant next to the wellhead is a floor under West Texas gas demand for two decades.

And Chevron isn’t only on the power side. The same week Kilby was announced, Chevron turned up on the partner list (alongside ConocoPhillips, Devon, and ExxonMobil) of a just-commissioned Western Midstream produced-water treatment pilot (they call it JIP 2) at Red Bluff Reservoir, in the same Reeves County where Kilby will sit. The facility turns oilfield wastewater into reclaimed fresh water suitable for, among other things, industrial cooling. To be clear: Western Midstream leads the project and Chevron is one of four consortium members, so this isn’t “Chevron single-handedly building water treatment.” But the facts line up like this: in one West Texas county Chevron is moving into both power and water at once, the two binding physical constraints of any AI buildout. The molecules that are worthless at Waha become a 20-year power contract; the wastewater that was a liability becomes a cooling resource. It’s hard to call that a coincidence: to my eye it’s strategy. The only caveat is that we’re inferring it from the facts, and Chevron has nowhere claimed it is “playing both sides.”

It’s worth sizing this against Chevron to judge how seriously to take the “new growth platform” framing. Chevron posted record 2025 production (3,723 thousand barrels of oil equivalent a day), $33.9 billion in operating cash flow, and its 39th consecutive annual dividend increase. Management is explicitly pitching power generation as a way to diversify cash flow and support those shareholder payouts. For a company that size, one $7 billion plant is not a pivot but a careful entry, an entry into a structural supercycle, and Chevron is moving while peers are still “talking about it,” as Gustavson pointedly noted.

So who actually won? Microsoft gets compute. Chevron, a long-standing player in the energy market, locks in a buyer for 20 years that it can’t easily lose (the plant is bolted to the campus; you can’t switch suppliers), places its most distressed product, and gets paid on the water side too. The turbine makers, GE Vernova and Caterpillar, book years of contracted orders. The overall pattern across this market is simple: the incumbent energy players and the equipment suppliers capture the bulk of the value, while the tech company carries the costs and the carbon.

The other workaround: a $227 million tax break

There is a second structure worth reading, and it sits on the tax side. When Texas replaced its old Chapter 313 incentive with the Jobs, Energy, Technology and Innovation Act (JETI) in 2023, the legislature wrote one guardrail plainly: data centers are not eligible, excluded by industry code. So the applicant here isn’t the data center. It’s the power plant. Energy Forge One, Chevron’s subsidiary, classified as electricity generation, filed JETI application J0022 through the Pecos-Barstow-Toyah school district, and the project filings put the break at more than $227 million over ten years, depending on the plant’s final size. The Comptroller recommended approval and the school board signed off in February; a final agreement still needs the Governor. Reporting describes it as the first JETI approval for a plant built to serve a data center.

It’s the SB6 sidestep one layer down: a rule written to exclude exactly this kind of project, cleared by the way the project is structured. A facility that exists to power a single data center, sells to no one else, and never touches the public grid qualifies for an incentive the data center itself could not get, because on paper it is a generator.

Two things keep this from being a footnote. The jobs: the application commits to “over 25 permanent, full-time jobs,” set against the “almost 2,000 jobs” in Chevron’s press release and the more than $10 billion in tax revenue the company also touts, even as its subsidiary lines up a $227 million break. And who pays: under JETI the state reimburses the district, so Pecos-Barstow-Toyah ISD, in one of the poorest counties in Texas, never feels the hole directly. The cost doesn’t vanish; it moves to the state budget, spread across every Texas taxpayer. Microsoft’s promise not to raise local bills was about electricity rates. It was never about this.

What to watch

This is where the analysis turns forward-looking and testable: every reassurance comes with a condition.

The ratio to watch is 1.33x. Chevron is building 2.67 GW of generation for a campus Microsoft describes as roughly 2 GW. This is a soft signal, not a smoking gun, and it’s important not to over-read it. Data centers are usually built with a reliability margin: in case some generators fail, you install spares, and on a plant of a few large blocks that margin can nearly double installed capacity. By that crude logic, 1.33x would look thin. But the margin doesn’t have to be twofold: Kilby is being built from seven GE Vernova turbines plus Solar Turbines units, and across many machines “what you need plus a couple of spares” is a premium closer to 1.4x than 2x. So 1.33x fits comfortably within a sensible reserve. The number is interesting mainly because it sits between regimes, and because the inputs are fuzzy: Microsoft doesn’t specify what “about 2 GW” means (IT load, or the whole facility including cooling?), and 2.67 GW is Chevron’s final, phased capacity, not its starting point. In short: this ratio is worth watching as the phases and the real load get disclosed, but on its own it isn’t a contradiction, especially since Gustavson said outright that the surplus will eventually flow to the grid.

Then there’s grid connection, and a myth worth killing. Microsoft says it will connect the plant to the grid “over time,” and Gustavson says the surplus power will be pushed to the grid to help stabilize it. It’s tempting to say: there it is, they’ll start selling surplus and raise the neighbors’ rates. In fact it’s the opposite. When generation is added to a market, prices go down, not up: the more supply, the cheaper for everyone. (David Sapper, vice president of transmission and markets at Clean Grid Alliance, rightly pointed this out in the comments.) The real risk to ratepayers is elsewhere, and it’s more important: when the plant interconnects, who pays for the grid upgrades needed to connect it? Those are large one-time costs, and SB6 is precisely trying to push them onto the large loads themselves, while also rewriting the formula for allocating transmission costs (decisions are due by the end of 2026). Put simply: the “we won’t touch your bills” promise holds cleanly only while the plant is fully islanded; the moment it joins the grid, the “who pays for the wires” question is back.

A few specific signals I’ll be tracking. The first is FID by the end of 2026: the whole pitch here is speed and certainty, so any slip or downsizing of the final investment decision would directly undercut that story, and the date is worth watching. The second is how the grid tie is actually built: surplus is already slated to flow to the grid, so the real question is scale. An interconnection sized mainly for backup import keeps the islanding story largely intact, while one built to sell power at scale quietly turns Chevron into an ERCOT generator, which is a different regulatory and political animal. The third is whether the plant’s water gets disclosed: it matters whether anyone ever puts a real number on its water draw rather than only the data center’s cooling, and continued silence will itself be an answer. And the fourth is permitting and the air fight: given the 13-million-ton CO₂ estimate and the xAI precedent in Memphis, where a far smaller plant drew an air-quality lawsuit, local and environmental opposition to Kilby’s air permits remains a live risk to the timeline.

And one last thing: the question the whole “Community First” framing talks around. Why do we need this much compute, this fast, and at this cost to one town’s air and water? Microsoft’s answer is customer demand and an AI revenue line growing 123% a year. Fair enough. But in many places the data center industry has earned a bad reputation, arriving loud, thirsty, and dirty before anyone answered the “why here, why now” question. “Community First” is largely a response to that backlash, and it’s worth watching whether it’s a real change in how these get built, or just a more polished version of the same playbook dropped into an oil-patch county that was unlikely to push back anyway.

The pattern

Pecos is a template, and Chevron’s own words (”in talks with other developers”) say it’s meant to be repeated. The schema is now legible end to end: behind-the-meter gas, wrapped in renewable-certificate accounting and a “community first” message, sited where regulation is lightest and resistance least likely. It solves the developer’s three hardest problems at once, speed, ratepayer optics, and regulatory risk, while handing an incumbent energy player a two-decade annuity on its most distressed product, a foothold on the water side of the same constraint, and, where the incentive rules allow, a nine-figure tax break on top.

That’s the realist read. In a room full of optimists cheering the AI buildout, it’s worth saying plainly: when the largest technology company on earth and one of its largest energy companies both call the same deal a win, the question isn’t whether AI needs the power. It’s who holds the 20-year contract. And in Pecos, that’s Chevron.

Sources: the Chevron and Microsoft press releases; reporting from Reuters, CNBC, the Los Angeles Times, Quartz, TechCrunch, DCD, The Register, Midland Reporter-Telegram, Utility Dive, the Charlotte Observer, and Latitude Media; the Environmental Integrity Project’s emissions estimate; Microsoft’s 2025 Environmental Sustainability Report; Western Midstream’s JIP 2 announcement; SB6 analyses (Baker Botts, Bracewell, McGuireWoods, Mayer Brown); the TCEQ air-permit application and the JETI application (Energy Forge One; Texas Comptroller, J0022) and EIP’s Oil & Gas Watch database; Waha pricing data (Natural Gas Intelligence, Reuters); BloombergNEF and Cleanview.

This piece is for informational and analytical purposes only and is not investment advice or a recommendation to buy or sell any security. All views and forecasts are the author’s own as of the date of publication and may prove wrong. Do your own research. Disclosure: as of publication, the author holds no position in any of the securities mentioned.

Awesome analysis, as usual. The JETI judo move is hilarious. Use the Force, Governor Abbott. You just got zapped by the training drone (allusion to the scene in Star Wars where Luke is training himself with the light saber and a laser-zapping drone).

I have two other questions/observations.

1. How sensitive is Meta to latency? This site is a very long ways from any population.

2. Another way to look at how this plays into Meta's net zero goals is that they are making use of gas that is waste. Historically, it would just have been flared, right? Or worse (from a climate change perspective), released straight into the atmosphere? So they are just taking advantage of what's almost a "free" (from a climate change creation perspective) fossil fuel and using it to make scads of power for our Instagram feeds.

3. When I look at that part of the county, what screams to me is the opportunity to inject truly meaningful amounts of wind and solar BTM. If it were Google, I bet that the gas plant would be providing maybe 30% of the energy. You could add batteries so the whole thing could be scheduled and the turbines run at full output/efficiency.